The machinery of copyright enforcement has traditionally focused on two vulnerabilities: the hosting layer and the advertising layer. Cut off a site's server, and it disappears. Cut off its advertising revenue, and it becomes unprofitable to maintain. Now a third pressure point is being systematised: the payment processor itself.

The Payment Processor as Enforcement Chokepoint

WIPO's latest initiative, Alert Pay, coordinates notifications to major payment providers like PayPal and Mastercard, flagging sites accused of copyright infringement or counterfeiting. The pilot phase reportedly resulted in a 71% removal rate for flagged merchant accounts. This is significant infrastructure pressure: a service loses processing capacity without a hosting provider being directly involved.

Payment processors operate under increasingly stringent compliance obligations. Visa, Mastercard, and PayPal maintain explicit acceptable-use policies that prohibit transactions related to copyright infringement. When a major rightsholder organisation files a complaint through an official channel like WIPO, payment processors face reputational and regulatory risk in ignoring it. The decision calculus is straightforward: terminating a disputed merchant account carries far less legal exposure than defending one.

Architectural Implications for Hosting Operators

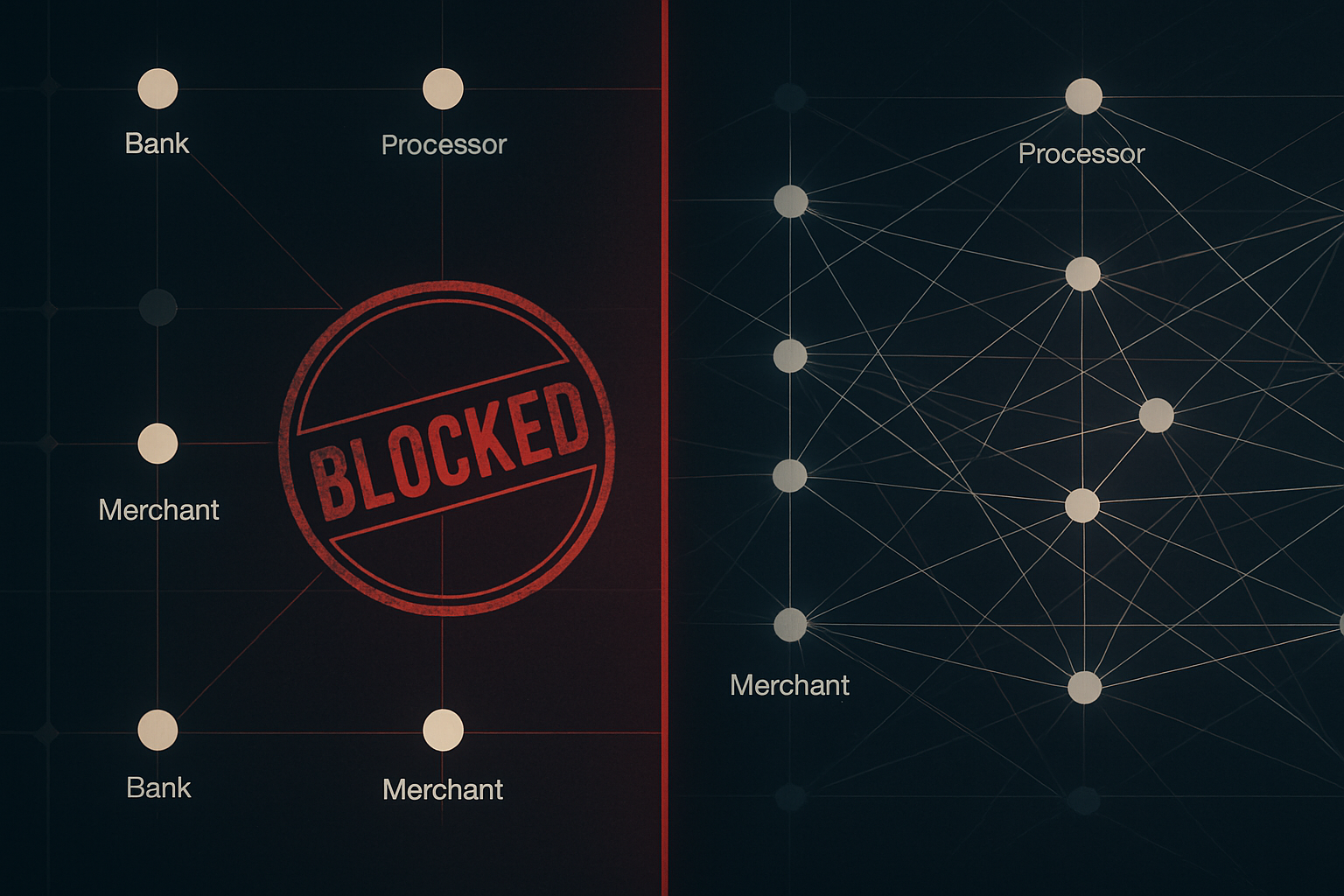

For hosting infrastructure professionals, this trend underscores a familiar principle: single points of failure are liabilities. Reliance on one payment processor—or payment processors from a single jurisdiction—creates unnecessary risk. A coordinated takedown campaign, whether WIPO-initiated or otherwise, can sever revenue flows regardless of the underlying hosting platform's legal status or technical robustness.

Operators managing services that may attract regulatory attention should assume payment processor churn. This means maintaining relationships with multiple providers before any incident occurs. Geographic diversification matters: processors bound by different regulatory regimes respond to pressure differently. Some jurisdictions have weaker copyright-enforcement coordination; others have no formal frameworks like WIPO Alert Pay. Similarly, cryptocurrency payment options introduce orthogonal infrastructure that does not depend on traditional financial networks.

The 71% removal rate in the pilot is high enough to warrant serious architectural planning, yet low enough that complete compliance is not guaranteed. Some merchants escaped removal—likely due to dormancy, contested claims, or processing complexity. This suggests payment processor termination, while effective, is not absolute.

Content Moderation Without Direct Legal Authority

What makes Alert Pay notable from an infrastructure perspective is its reliance on private-sector enforcement without judicial process. Payment processors apply their own policies to WIPO's flagged list; there is no court order, no formal legal judgment. This is a contractual enforcement model, not a legal one. The processor acts as an enforcement agent based on terms of service and risk assessment, not statutory obligation.

For hosting infrastructure, this means the legal posture of a given service matters less than the commercial compliance preferences of its payment partners. A service operating in full legal compliance in its jurisdiction can still lose payment processing if a major processor—acting on WIPO's complaint—decides the reputational risk exceeds the business value.

This dynamic has been present for years in advertising networks (which routinely cut off publishers based on rightholder complaints), but formalising it at the payment layer increases the pressure significantly. Advertising can be replaced; payment processing is harder to substitute quickly.

Jurisdictional Arbitrage Limits

Operators have traditionally relied on offshore hosting or privacy-focused jurisdictions to avoid copyright enforcement. Hosting infrastructure in countries with weak DMCA enforcement or no formal international copyright cooperation used to provide meaningful protection. Payment processor networks, however, are globally consolidated. Visa and Mastercard operate internationally, and participating payment processors in virtually all jurisdictions adhere to their compliance frameworks.

This means jurisdiction shopping no longer provides the protection it once did. A service hosted in a non-cooperative jurisdiction can still lose payment processing through coordinated processor pressure. The financial infrastructure layer has become the real enforcement bottleneck.

Closing Thoughts

WIPO Alert Pay formalises a trend that was already underway: payment processors are the most effective non-judicial enforcement mechanism available to rightsholders. For anyone managing hosting infrastructure, the lesson is pragmatic. Build payment redundancy into your architecture before it is needed. Maintain relationships with multiple providers, explore geographic alternatives, and understand cryptocurrency integration not as speculation but as operational resilience.